Do Central Bankers Know What They're Doing?

In North America, the problem faced by central bankers beginning in 2021 was unprecedented. How could the Fed and the Bank of Canada engineer a disinflation in a regime with inflation targeting, with an overnight nominal interest rate as an intermediate target? It’s been a struggle, but things have gone surprisingly well. Unfortunately, central bank officials seem at a loss as to how to close the deal.

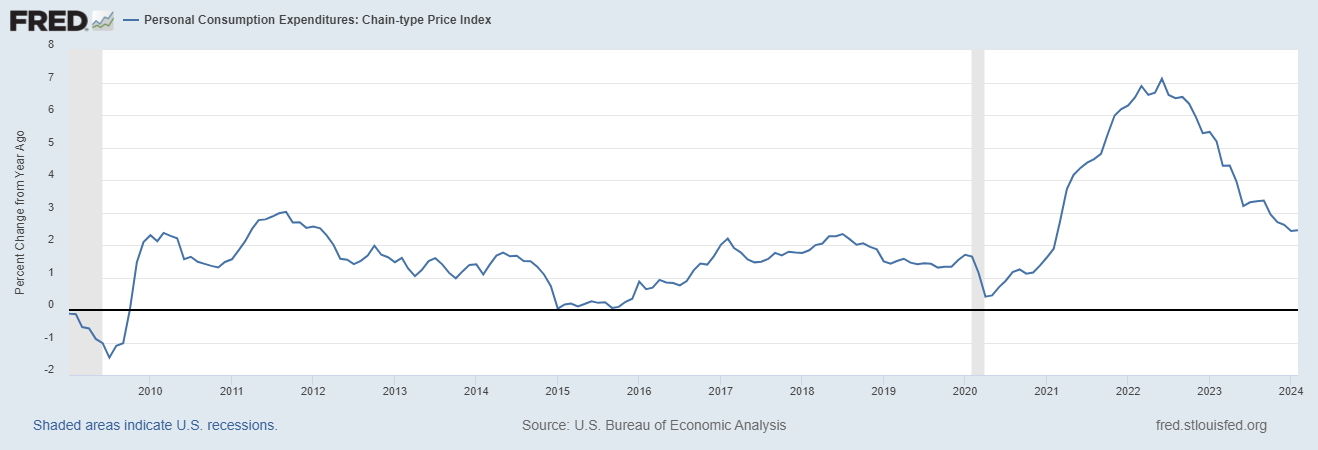

Let’s start with the state of affairs in the U.S. Not everyone seems to know this, but the FOMC claims that it is targeting the PCE deflator. By that measure, inflation is essentially at target, as these things go:

The last observation in the chart is 2.5%. People looking for evidence to support their personal narrative can of course find other inflation measures to make their case, but typically there’s little in the way of theory or empirical evidence to support looking at anything other than the measure the Fed chose.

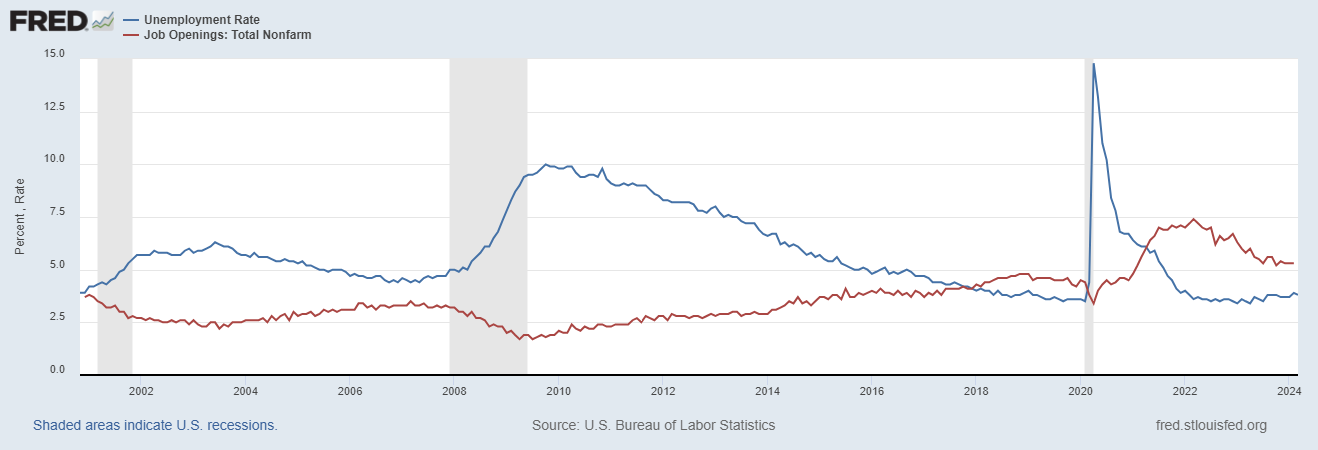

On the real side, the labour market is less tight than it was, but the numbers are still showing strength:

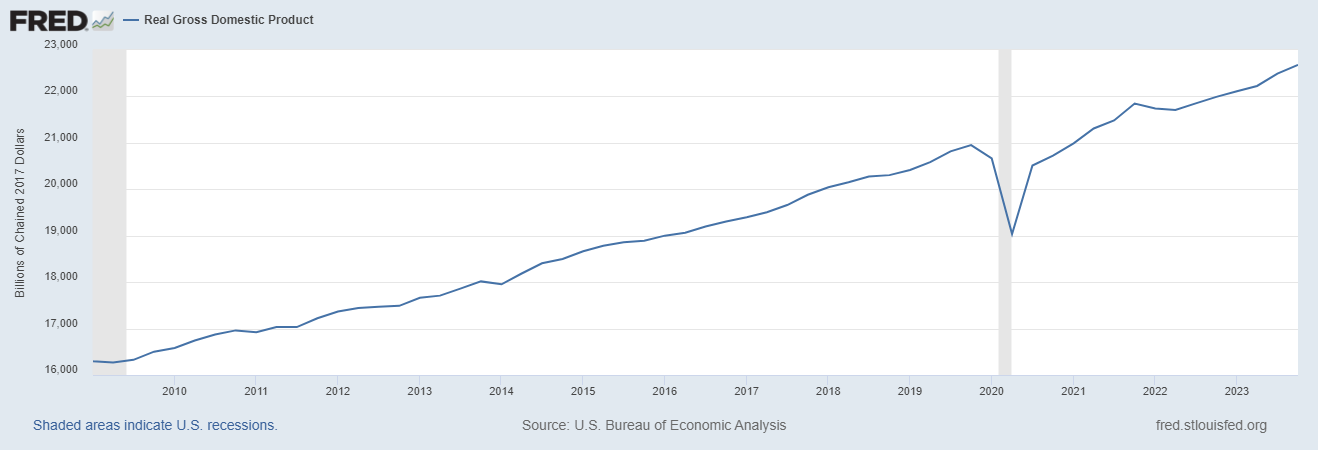

And real GDP is growing at a good clip:

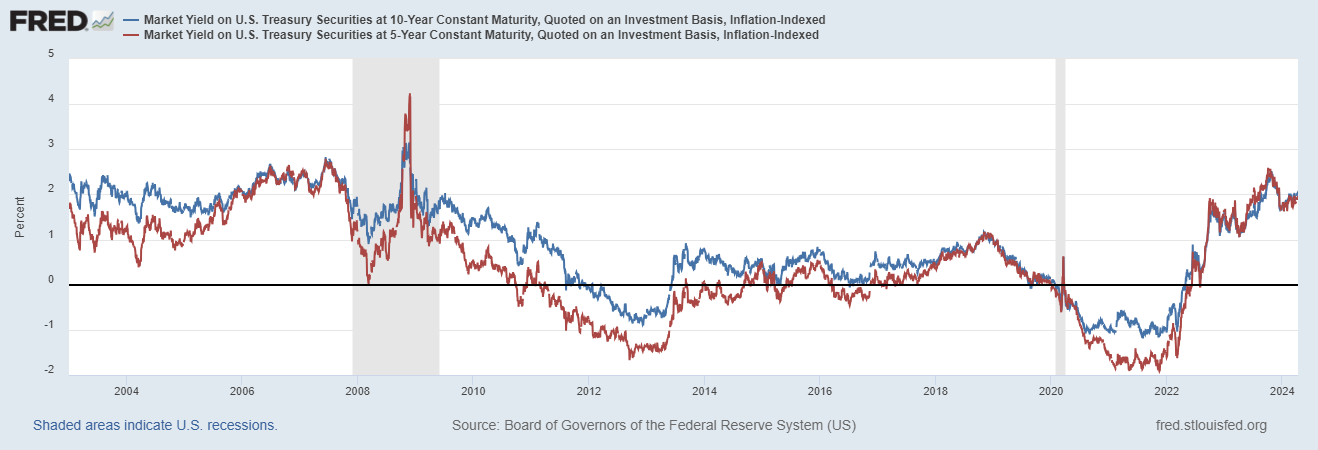

As well, to the extent we can measure anticipated inflation, that’s under control, as evidenced by 5 and 10-year breakeven rates, which are about where they were before the financial crisis:

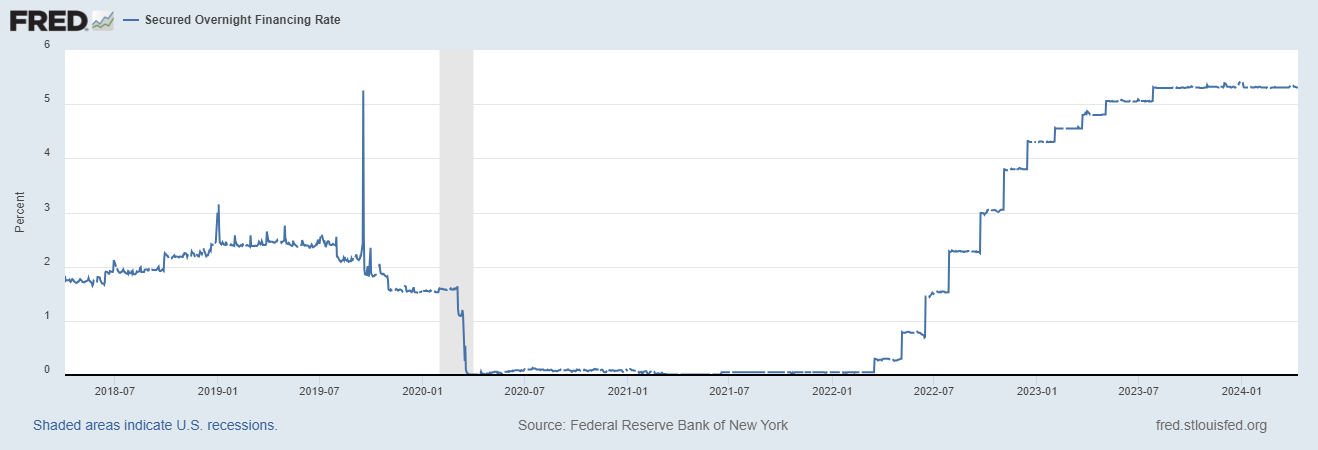

So, the state of the U.S. economy, by these measures, appears to be as close to perfect as the FOMC might want, given its dual mandate, including its 2% PCE inflation target. Then, given that the median FOMC member still thinks the long-run nominal interest rate should be about 2.5%, if I had been asleep for 20 years, just woke up, looked only at these charts, and knew the 2.5% long-run estimate, I would wonder why the overnight rate was not 2.5% instead of 5.3%.

[And note - here’s another beef - that I’ve plotted the secured overnight financing rate, as that is what the Fed is currently targeting. Basically, the Fed’s setting for the interest rate on its reverse repo facility currently determines the overnight repo rate. The Fed claims to be targeting the fed funds rate “in a range,” but that’s bullshit.]

So, what could the FOMC people be thinking? They’re all eager to be Paul Volcker, or what? Maybe they’re worried about CPI inflation, which was up to 3.5% year-over-year in the last report. But, again, CPI inflation is not what the FOMC chose to target. My best guess, though, is that the FOMC isn’t so worried about the actual inflation numbers as the state of the real economy. That is, the idea that the inflation rate is controlled by controlling the unemployment rate persists at the Fed, as it does at most central banks in the world, despite plentiful evidence to the contrary. Fed officials were fond of telling us, pre-Covid, how the Phillips curve was “flat” (perhaps “nonexistent” would have been a better word), but that didn’t stop some people (notably Larry Summers) from claiming that to bring inflation down from where it was in mid-2022, we needed a long period of high unemployment. Well, apparently not. Inflation came down with essentially no upward movement in the unemployment rate. The Phillips curve narrative persists, as it somehow allows monetary policy committees to achieve consensus, and it’s easy to explain to the public - however wrong it may be. Unfortunately, if central bank officials speak Phillips curve language for long enough, they start to believe it, which produces bad monetary policy.

The job of the FOMC going forward is to invent a narrative that allows them to justify bringing the overnight nominal interest rate down to something commensurate with 2% inflation in the long run. That may be an overnight rate of 2.5%, but it could be higher. I haven’t been impressed with existing models of the long run real interest rate, but U.S. TIPS yields may indicate that the long run real rate has risen:

This might tell us that the long-run real rate is closer to 2% than to 0.5%, the FOMC consensus. If so that’s good news for inflation targeting. That is, if the policy rate stayed at 5.3% forever, and the long-run real interest rate is 2%, then we would expect inflation to come in at 3.3%, which is better than 4.8% under the FOMC consensus.

The bad news is that the FOMC, along with other central bankers in the world, may be setting itself up for persistent overshooting, just as central banks tended to undershoot their inflation targets from 2010 to 2020. That’s all part of the same phenomenon, which is not recognizing long-run Fisher effects - and this may set in sooner than people seem to think. Basically, consistent with all mainstream macroeconomic theory, a persistent increase in the central bank’s nominal interest rate target produces a long-run increase in inflation, not a decrease. What allows a central bank to hit its inflation target is a widely-held belief that the central bank will always revert to a nominal interest rate target consistent with its inflation target and Irving Fisher. If that widely-held belief falters, the game’s up.

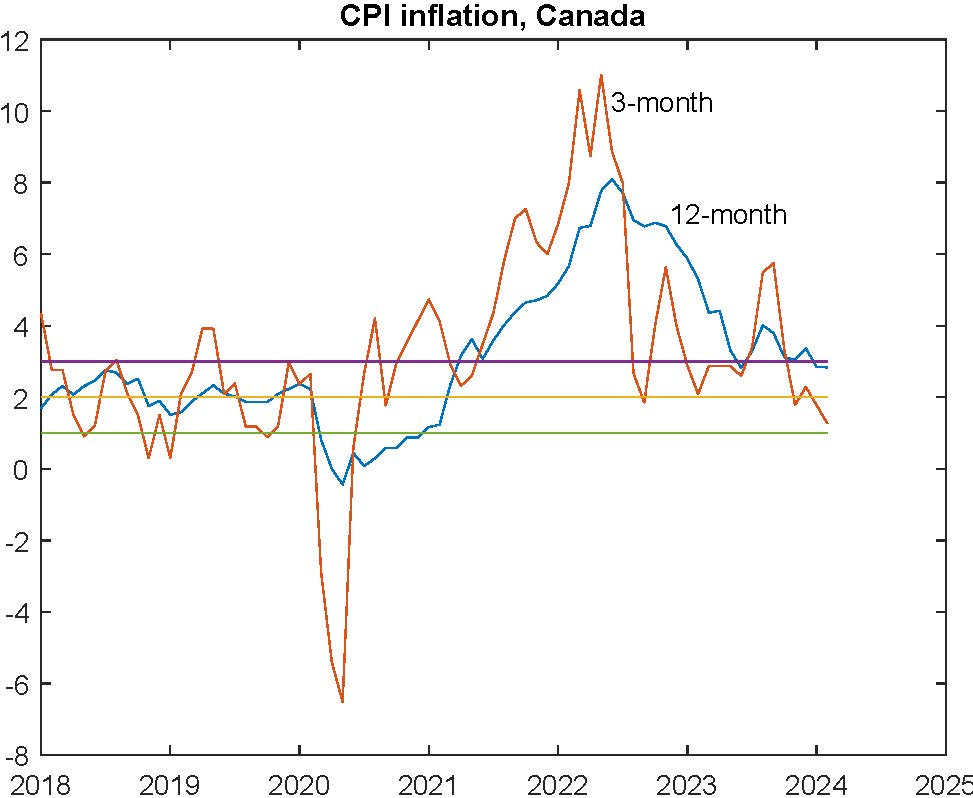

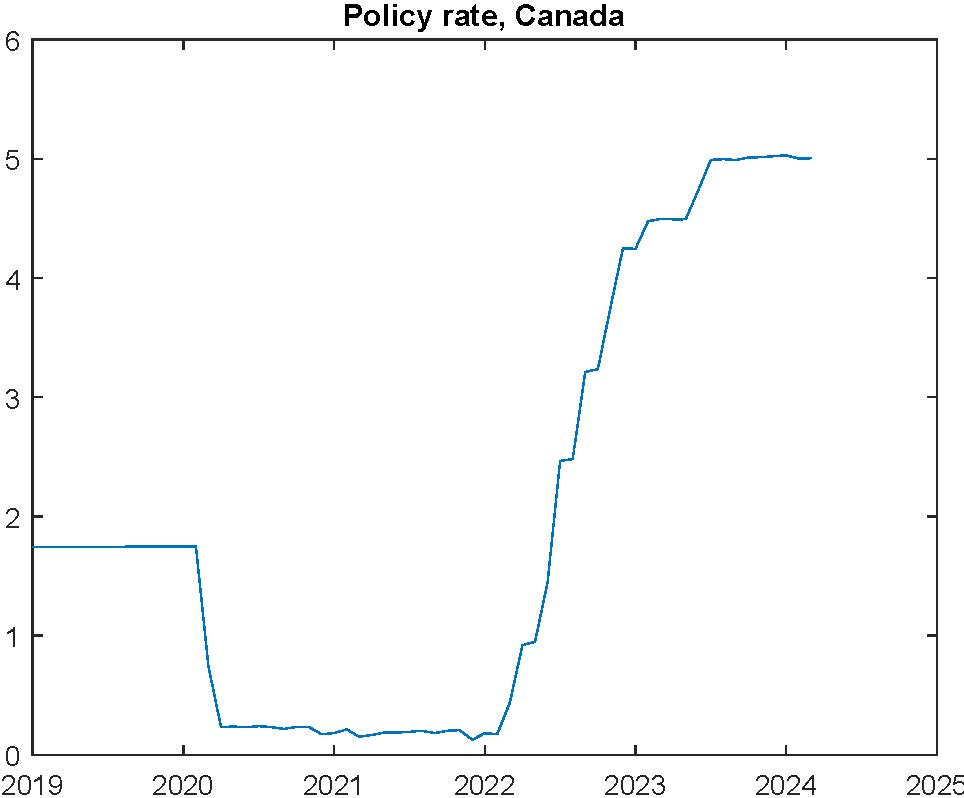

As is typical, the macroeconomic situation in Canada is not so different from the U.S., though the case here is even stronger for interest rate cuts. Canadian CPI inflation is now within the Bank of Canada’s 1% to 3% target range for 12-month inflation, and 3-month inflation rates have fallen below 2%:

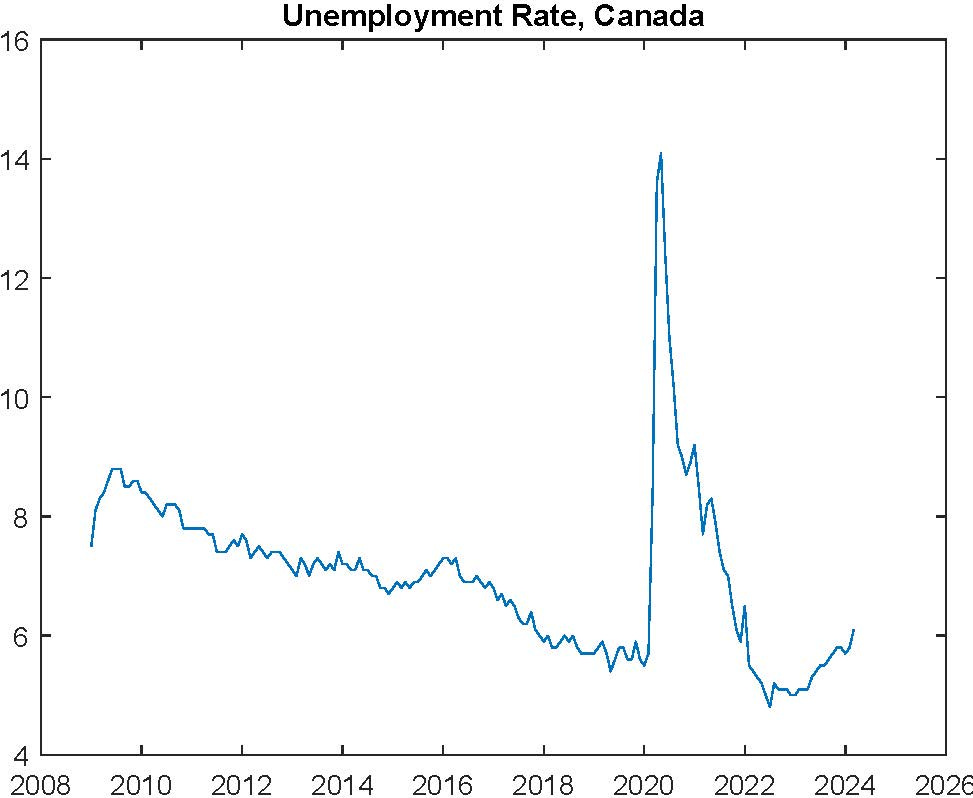

Though employment growth is high, the unemployment rate has increased recently:

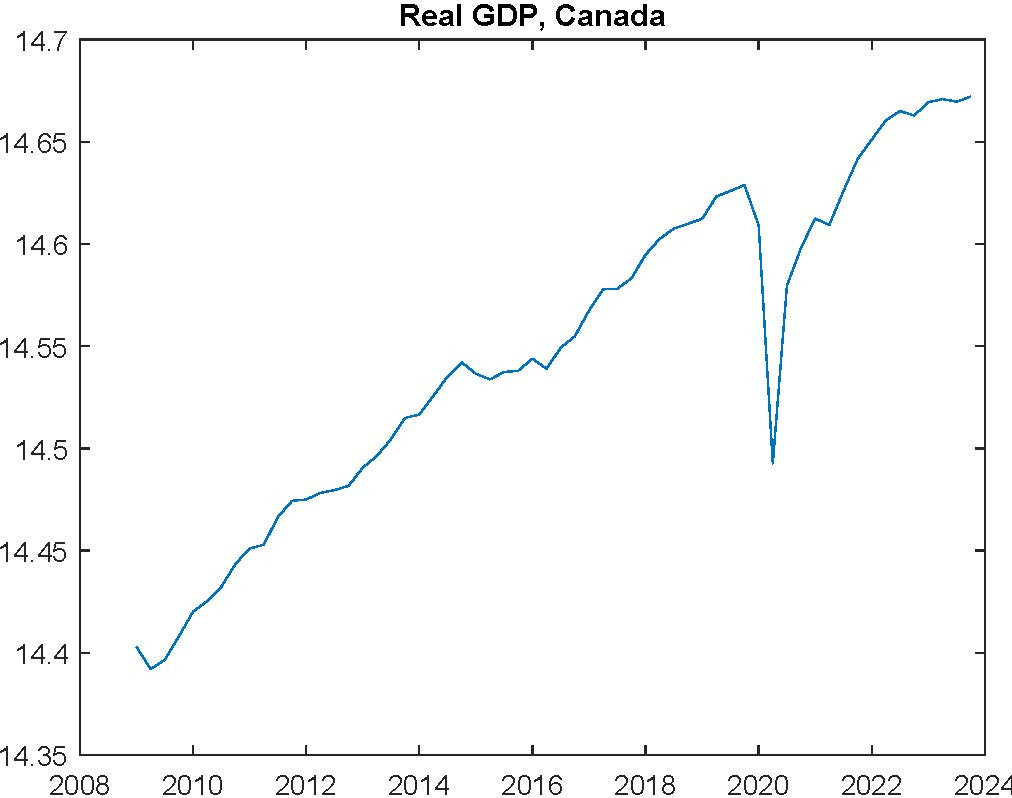

Real GDP growth is somewhat anemic, in part reflecting poor productivity growth:

So, inflation performance is good, the real economy is weakening, but the Bank of Canada persists with a policy rate of 5%, in spite of its own estimate of a “neutral” nominal interest rate of 2% to 3%:

Again, central bankers seem to think that they have all the time in the world to contemplate whether or not to reduce their nominal interest rate targets. But, as usual, doing nothing amounts to something, and it’s not good. Stop dragging your feet, folks!