Is this high-inflation episode over, or what?

Answer: Given current policy, and where it appears to be headed, I don’t think so.

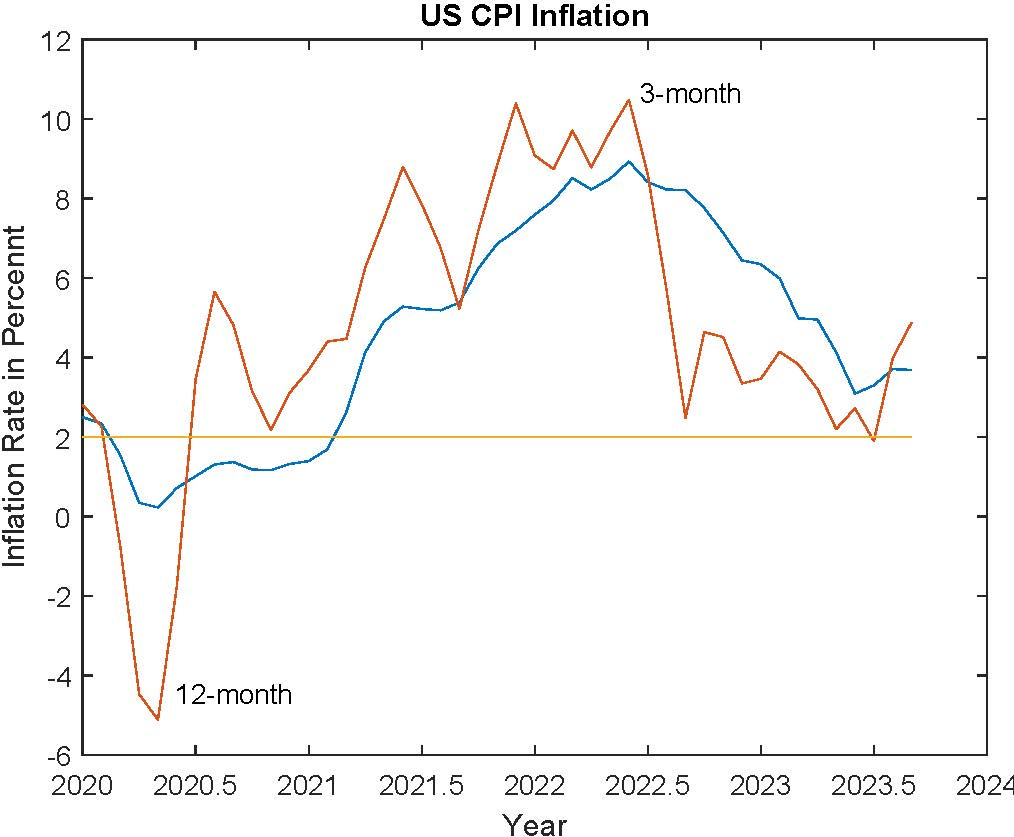

First, let’s review where we are, in terms of inflation. In the US, 12-month and 3-month headline CPI inflation rates look like this:

So, things have certainly improved from mid-2022, but the 12-month CPI inflation rate is still well above 2%, at 3.7% in October. And the 3-month CPI inflation rate is certainly not coming down, which is troubling. I’m focusing here on CPI inflation, rather than PCE inflation, which is what the FOMC claims to be explicitly targeting, so I can draw a better comparison to Canada.

At this point you may wonder why I wouldn’t look at core measures of inflation - measures with volatile prices stripped out in various ways. I think there are good reasons to ignore core measures. One typical justification for looking at core measures is that they are claimed to forecast headline measures of inflation. So, first, I’m not sure that’s correct. Here’s headline CPI inflation CPI inflation ex food and energy for the US:

So, eyeballing that chart, I’d say it looks like headline leading core, not the reverse. Second, if what you are interested in is forecasting future headline inflation, I think you could do a better job by using all the available information, rather than stripping some prices out of the headline index and using that. Finally, there’s no theory that gives us any confidence in a specific core measure. I understand the motivation, which is to try to look past volatility in the headline inflation measures, but I don’t think this works well in practice.

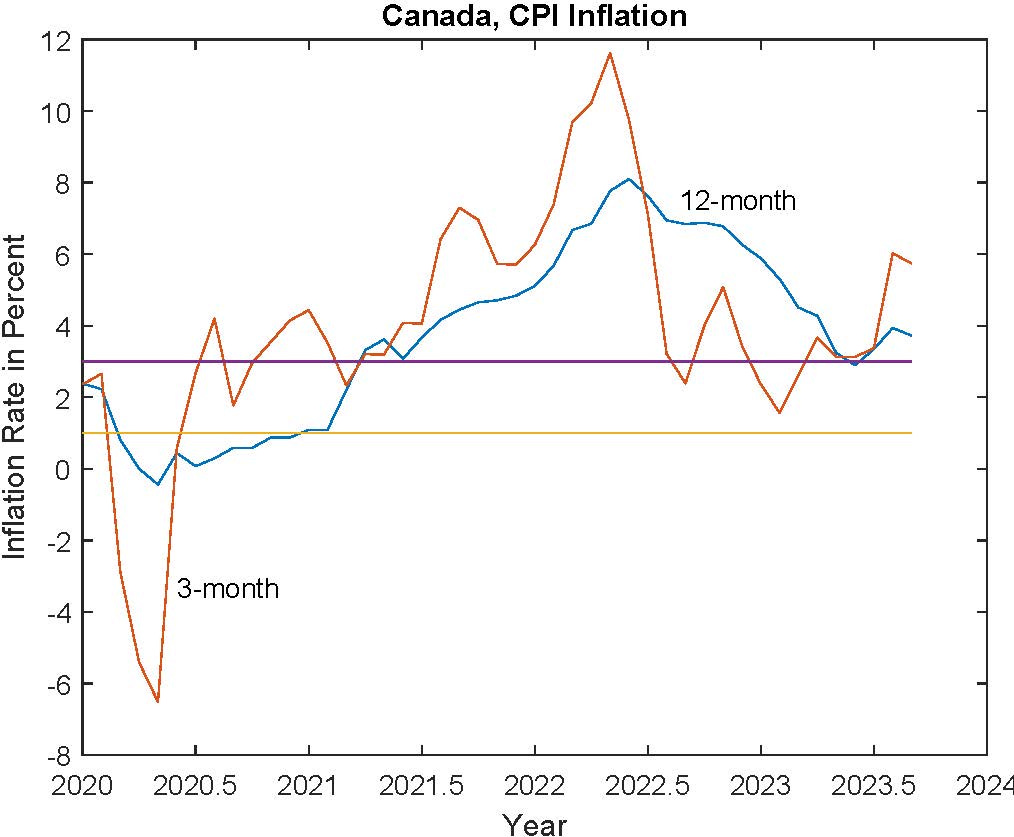

Anyway, on to what’s going on in Canada:

So, that’s essentially the same story as in the U.S. I’ve showed the Bank of Canada’s 1-3% target range for headline CPI inflation. As in the U.S. 12-month inflation has come down substantially, but it’s still above the target range, at 3.7%, and the 3-month inflation rates are not coming down.

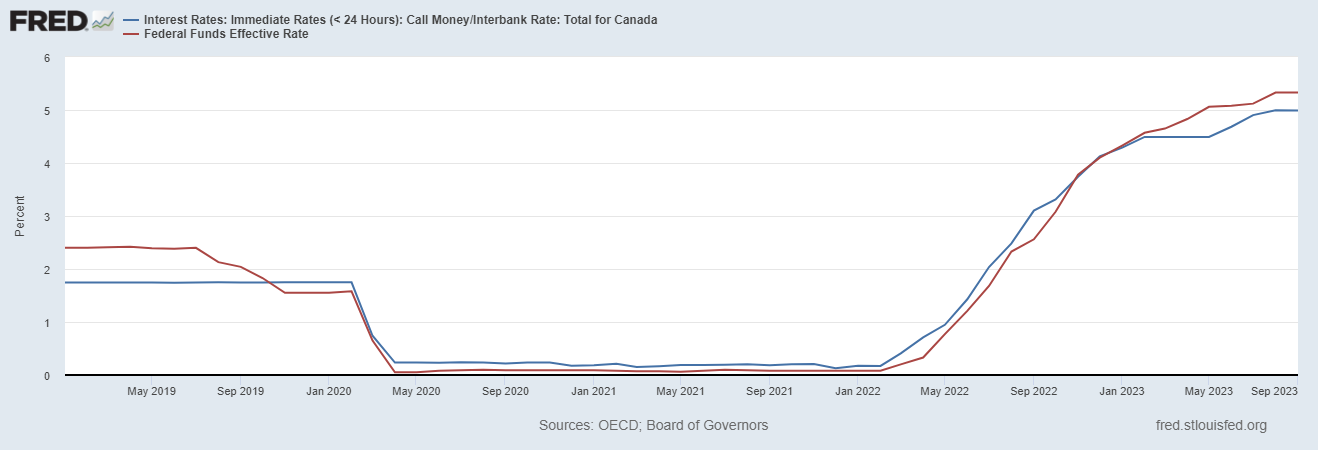

So, what have the Fed and the Bank of Canada been doing?

I’ve shown overnight rates in the two countries, which are more or less the same. The Bank of Canada began interest rate increases earlier in 2022 than did the Fed, but did not go as high - the overnight interest rate in Canada is about 30 basis points lower than the effective fed funds rate.

We’ve seen so far that U.S. and Canadian experience during this hig-inflation episode is quite similar, both in terms of the problem, and the monetary policy response to the problem. And, the narrative that BoC officials and Fed officials spin is very similar as well. Basically, according to these people, a disinflation is produced by high interest rates. “Demand” is too high relative to “supply,” an increase in the nominal rate of interest increases the real rate of interest, which reduces demand, which reduces the rate of inflation. It’s basically an IS/LM/Phillips curve story.

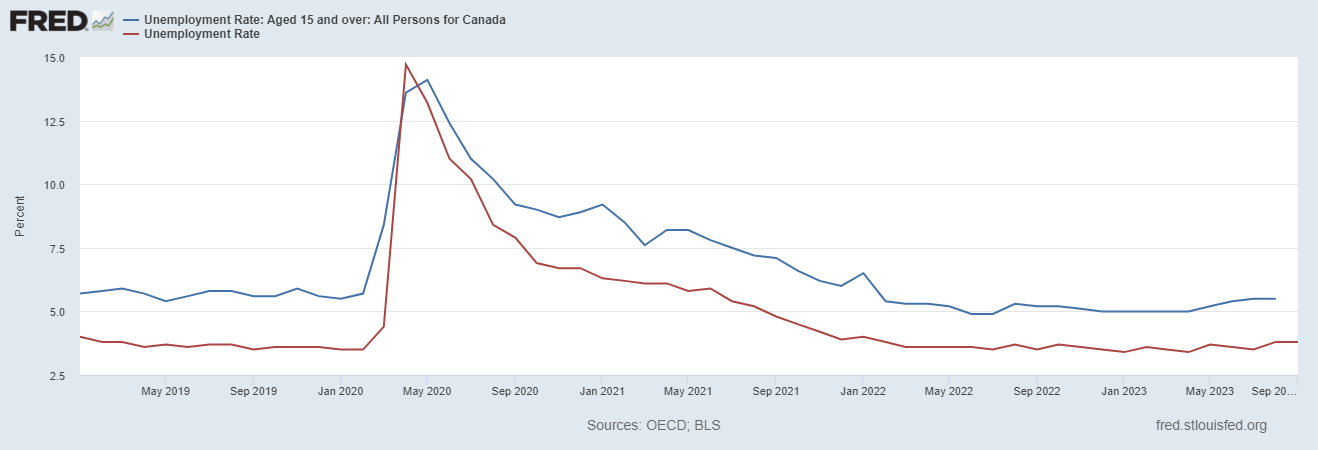

So, how does that narrative mesh with what has actually occurred? There’s been a disinflation alright, but here’s what’s been going on in labor markets:

There’s been a slight increase recently in the unemployment rate in Canada, but unemployment rates in both the U.S. and Canada are still in the ballpark of where they were pre-pandemic. So if the central bank narrative is correct, why did inflation come down? In the basic narrative that reduction in demand shows up as a decline in economic activity and an increase in the unemployment rate - it’s not something I can’t see. So, if we believe the narrative, then the inflation rate actually came down on its own. Whatever made it go up - and there’s certainly no consensus about that, other than that it’s pandemic-related - those factors worked in reverse to make inflation come down. So, that’s troubling, as it says that it’s possible that central banks could have done nothing and been in the same place - or better possibly.

But what about the standard narrative? Does it make any sense? Let’s go way back - to the Volcker era in the U.S. When Volcker became FOMC chair, in 1979, inflation was high, and there was a consensus that something needed to be done about it, though there were differing views about how to engineer a disinflation (monetary policy vs. wage and price controls, essentially). Volcker’s FOMC seemed convinced that monetarist principles would work - follow a Milton Friedman prescription of reducing money growth, and inflation would surely come down.

So, if we think of monetary policy as managing money growth, the idea is that we ignore the path of interest rates, reduce money growth, and hope for the best. A worry in the old days was that non-neutralities of money - sticky wages and prices, credit market effects, whatever - would kick in, and we could suffer a long period of high unemployment. But that would be a symptom of disinflation. Ultimately, long-run neutrality tells us that, if we wait long enough, then inflation and nominal interest rates will be low, and the real economy will be humming along.

Fortunately, though the 1981-82 recession was relatively severe, inflation fell, nominal interest rates fell, and by the mid-1980s the U.S. economy was humming along. But central bankers’ interest in monetarism didn’t last long, as money growth targeting proved to be a poor approach to ongoing inflation control. So, what evolved is what we have now, in most countries: a central bank with an inflation target, with the primary means for achieving the target being some implicit policy rule for adjusting a nominal interest rate target, given observables.

But, given this modern framework for monetary policy, central banks have a rather strange view of how inflation control works. For example, central bankers want to engineer a disinflation not through some means where we know where we’re going in the long run (low inflation, low nominal interest rates, economy humming along), and anything bad that happens is due to non-neutralities of money. Instead, they seem to think that disinflation works through the non-neutralities of money, as if Volcker reduced inflation because he induced a recession. Basically, we control inflation by controlling the unemployment rate. And we’ve known for a long time that that’s a messed-up approach - or maybe some people forgot.

The danger here is the following. Long-run neutrality - inherent in all the dynamic models we work with, essentially - says that higher nominal interest rates ultimately engender higher inflation. That’s just Irving Fisher. That’s why the long run world with low inflation has low nominal interest rates. So, in a disinflation, engineered by the modern central banker, that central banker eventually has to find a reason to reduce nominal interest rates. What would make our central banks cut interest rates? More unemployment? Inflation at target? Both?

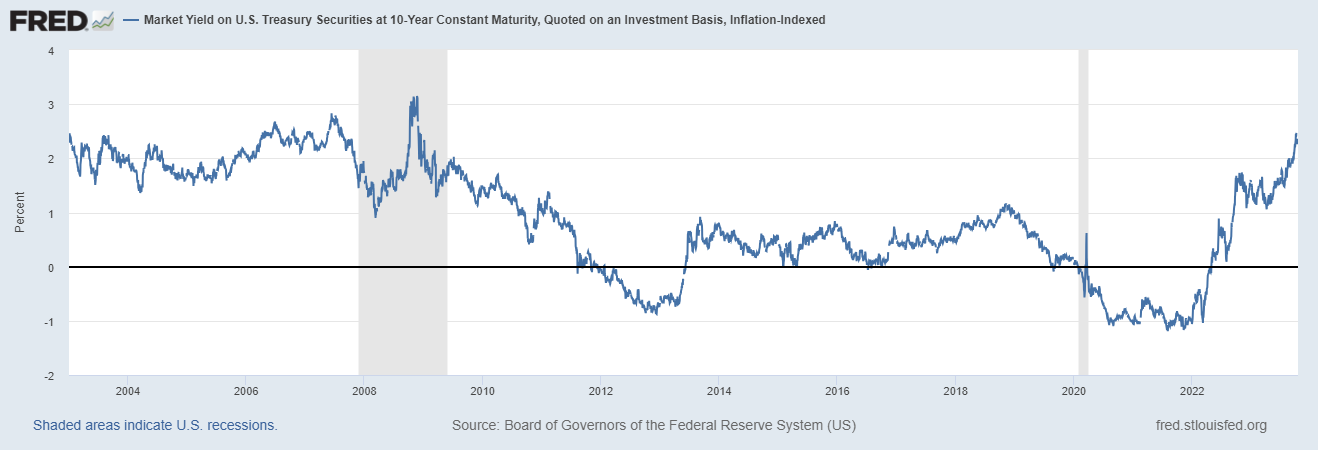

The risk is that, if high nominal interest rates persist, then so does high inflation. How high? Well, this data is encouraging in that respect:

This is the yield on U.S. 10-year Treasuries, inflation-indexed. This is now above 2%, about where it was just prior to the financial crisis. Canadian and U.S. central bankers, the last I checked, seem to think that the long-run short-term real rate of interest is in the range of 0% to 1%. So, for example, if nominal interest rates persist at about 5%, then we should ultimately see inflation in the range of 4% to 5%. But suppose, in line with the above chart, that the long-run real interest rate is about 2%. That means long run inflation of about 3%, given a 5% nominal interest rate - not so bad, though still not at target.

Serious disinflation is something that has never been done before in the context of modern central banking frameworks (inflation targeting and nominal interest rate rules). I wish I were more confident in BoC and Fed people, but they worry me.

Seems like the answer was yes

"So, if we believe the narrative, then the inflation rate actually came down on its own. Whatever made it go up - and there’s certainly no consensus about that, other than that it’s pandemic-related - those factors worked in reverse to make inflation come down. "

This makes the rise and then fall in inflation understandable!

https://marcusnunes.substack.com/p/a-monetary-policy-whodonit