Renewal of the Bank of Canada's Inflation-Targeting Agreement with the Government of Canada

I wrote a piece for the C.D. Howe Institute in April 2021, making the case that the Bank of Canada should keep the then-existing agreement with the government in place, without amendments, when the time came to renew the agreement. So, the time has come and, indeed, the new agreement is more or less the same as the old one, in terms of the specifics. In practice, this could make little difference for actual Bank policy actions. But the new agreement certainly is not an improvement, as it adds vague and unnecessary language that most people will find hard to understand.

So, at its core, the agreement says:

The target will continue to be defined in terms of the 12-month rate of change in the total CPI.

The inflation target will continue to be the 2 percent mid-point of the 1 to 3 percent inflation-control range.

The agreement will run for another five-year period, ending December 31, 2026.

That’s been the fundamental part of the agreement since 1991. It’s important to recognize what’s useful about this as a central banking goal. Basically,

It’s easy to understand what the Bank’s goal is.

It’s simple to evaluate the Bank’s performance relative to the goal.

The bank is capable of performing well relative to the goal, based on what we’ve observed for the last 30 years.

If the Bank performs well relative to the goal, this arguably is the best the Bank can do, relative to any other goals it might specify.

The trouble is in part with this:

“The Government and the Bank also agree that monetary policy should continue to support maximum sustainable employment, recognizing that maximum sustainable employment is not directly measurable and is determined largely by non-monetary factors that can change through time.”

So what’s “maximum sustainable employment?” The language here does not help me understand what the concept is, nor how to measure it. Indeed, we’re told that it’s “not directly measurable.” So there seems to be a goal here, but it’s ill-defined, and the agreement is up-front that we’re not going to be able to evaluate the Bank’s performance in achieving maximum sustainable employment, whatever that is. So why put that language in there?

And there’s more information here:

“Major forces, including demographics, technological change, globalization, and shifts in the nature of work, are having profound effects on the Canadian labour market. These evolving forces have increased uncertainty about the level of maximum sustainable employment (i.e., the level of employment beyond which inflationary pressures arise).”

So, again, if all these evolving forces have increased uncertainty about maximum sustainable employment, why are we even talking about it? This passage does, however, attempt to define what the concept means which is “the level of employment beyond which inflationary pressures arise.” So, that sounds something like the natural rate of unemployment. But how would this help us think about what we saw in the 1970s, or what we’re seeing now? In the 1970s, seemingly we saw “inflationary pressures” arising when employment was low and unemployment was high. And, currently, the Bank is on the record expressing the view that, in spite of the fact that there seems to be a lot of inflationary pressure, and actual inflation, there’s still slack in the economy, which Bank officials seem incapable of defining or measuring. So, apparently, maximum employment is not necessary for inflationary pressure. If you’re now hopelessly confused, it’s not your fault.

Here’s another issue:

“The Bank will also continue to leverage the flexibility of the 1 to 3 percent range to help address the challenges of structurally low interest rates by using a broad set of tools, including sometimes holding its policy interest rate at a low level for longer than usual.”

A lower-for-longer policy is what the Bank signed on to last year. Here’s the relevant language in the December 8 press release:

“We remain committed to holding the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved.”

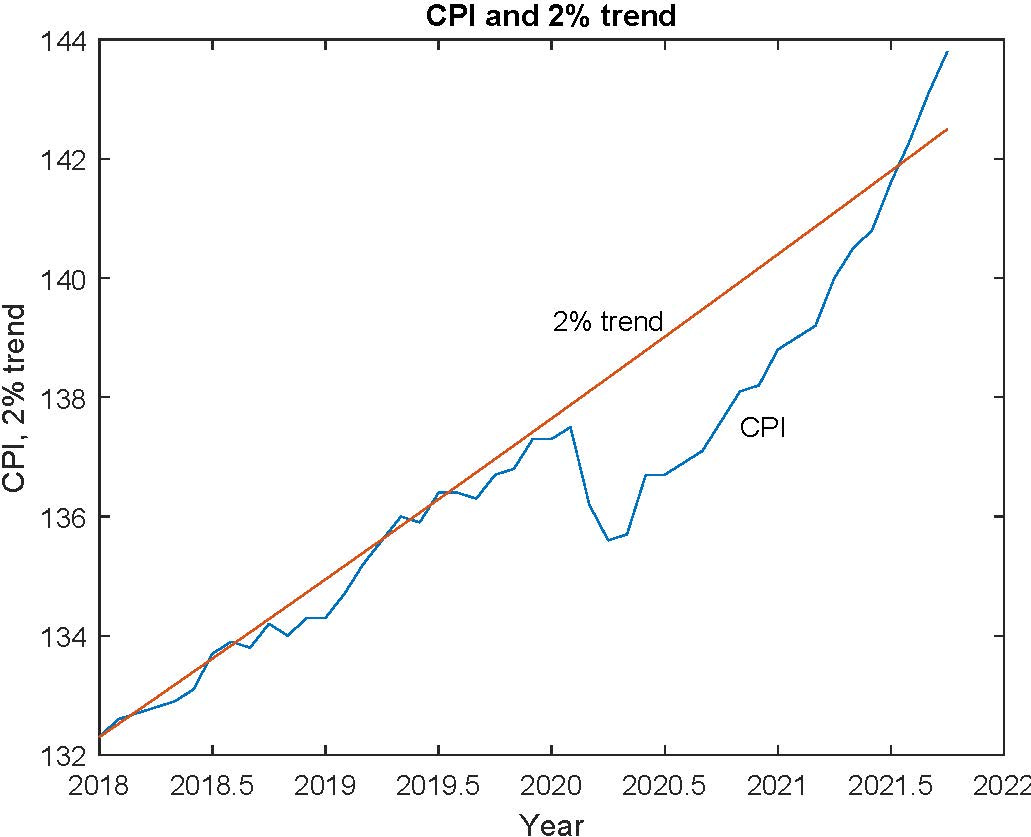

So, that commitment hasn’t panned out well. The passage reads as if the Bank is controlling “economic slack” - presumably a negative deviation from maximum sustainable employment - so as to control inflation in the long run. But here’s what the path of the consumer price index looks like, from January 2018, relative to a 2% inflation path (I think this is up to date - Statcan is currently down).

So, the Bank’s notion, given the Phillips curve model that seems deeply embedded in Bank officials’ minds and in this agreement was that, coming out of the pandemic, inflation would return to the 2% target from below, as the economy returned to maximum sustainable employment. But of course, that didn’t happen, leaving the Governing Council confused about what to do, other than to stick to their commitment to do nothing until next year. And note that one could even make a case that we’re currently at maximum sustainable employment, given the November labour force data.

So, we can now see the Bank performing badly, relative to its primary stated goal, but doing nothing about it, because they made an unwise commitment last year of lower-for-longer. But in spite of the fact that lower-for-longer now looks questionable, there it is in the new inflation-targeting agreement.

I won’t say this new IT agreement is surprising, as it reflects a standard inclination of central bankers, which is to invest excessively in words that serve only to confuse people. I think I know why the new language is there - which is to placate one or Governing Council members with strong ideas about dual mandates. But the additions don’t serve any useful purpose, unfortunately.