The Fed's Policy Implementation Framework Does Not Work As Advertised. How Come? Part I

The floor that's not a floor.

[This is long enough that it exceeded Substack’s email length limit, so I’ve split it in two parts. Part II here.]

Given recent events in the US overnight credit market, this is a good time to re-assess the Fed’s current approach to implementing monetary policy. This is a topic that some people think is just a matter of some technical details, but I think it is much more important than that. Thinking about this helps us understand quantitative easing (QE) and its effects, and I think reveals important aspects of how conventional monetary policy works.

The Poole Model, and How the Fed Uses it to Think About Implementation

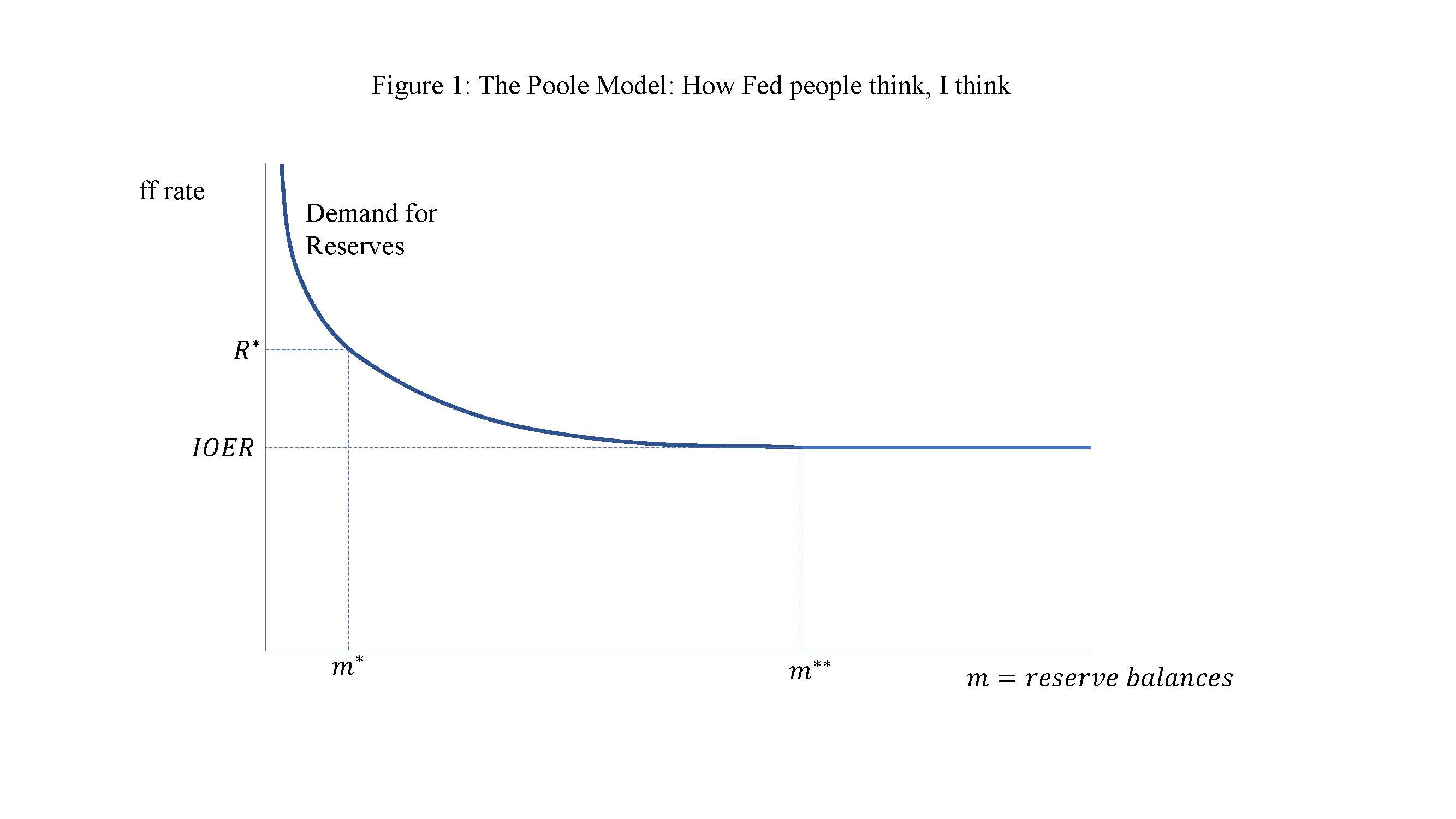

The people at the NY Fed have a particular view of how monetary policy implementation works, with and without a large central bank balance sheet. You can find this theoretical apparatus in any number of notes and staff papers written in the Federal Reserve System. Here’s how it goes. We’re supposed to think of monetary policy implementation - fulfilling the directive of the FOMC to hit a target for the fed funds rate - in terms of a partial equilibrium model of the market for overnight reserves. Looks like this:

So, the narrative that typically goes with Figure 1 is that, before the financial crisis, when the Fed ran what’s typically considered a “corridor” system, each day the people running the Open Market Desk at the NY Fed would need to figure out what the demand curve for reserves looked like, then inject the required quantity of reserves into the market. In the figure that quantity of reserves is m*, which then pegs the fed funds rate at R*, provided of course that the NY Fed people are good at predicting the demand for reserves, based on the day, the month, and inside information they may have had about disturbances in the overnight market. In a corridor regime, the interest rate on reserves, or in this case the interest rate on excess reserves - IOER in Figure 1 - is set below the interest rate target R*. For example, before the financial crisis, IOER = 0 in the United States.

But, according to this thinking, the corridor system involves implementation with “scarce” reserves. Alternatively, the Fed could run a “floor” system, which in this modeling framework means that IOER puts a floor under the fed funds rate. If reserves are sufficiently “abundant,” that is m > m**, then through arbitrage in the overnight market the fed funds rate is pegged at IOER. This is where the view that the floor system makes policy implementation “easy” comes from. Figure 1 makes you think that the corridor system is hard, requiring a lot of work to forecast reserve demand and then, with inevitable errors in forecasting, there is some variability in the market fed funds rate from day to day. A floor system is “easy,” as all that has to be done is to administratively set IOER, and arbitrage looks after the rest. With the floor, all the Fed has to be seriously concerned with is what m** is, apparently. Figure that out, and you’re done.

After the financial crisis, there seemed to be a view at the Fed that the floor system was temporary. The Fed would intervene with unconventional asset purchases, making the floor approach a necessity - the Fed wasn’t thinking about simplicity, their unconventional large-scale asset purchases were going to result in m > m**. So, the Fed moved up the introduction of the payment of interest on reserves to fall 2008, so that tightening could happen in the future, when appropriate, by increasing IOER. Otherwise, the Fed would be stuck at a zero fed funds rate, until sufficient assets matured or were sold, or the demand for currency grew sufficiently.

But in 2017 the Fed decided that it would continue indefinitely with its floor system. Why? Well at that point, the FOMC had convinced itself that the floor system made life easier. Indeed, that was part of what Bill Dudley, then the President of the New York Fed articulated in a speech in April 2018 (see also George Selgin’s piece relating to Dudley’s speech). Dudley said:

“In my view, the case for retaining the current floor system is very compelling for a number of reasons. First, it is operationally much less complex than a corridor system. In the current regime, the setting of IOER is largely sufficient to maintain the federal funds rate within the FOMC’s target range, as we have seen over the past few years. In contrast, a corridor system requires forecasting the many exogenous factors that affect the amount of bank reserves outstanding, and then engaging in open market operations on a near daily basis to keep reserves at a level consistent with the FOMC’s target range. This task would likely be more difficult now because of greater fluctuation in these exogenous factors relative to when the corridor regime was last in place.”

So, what’s wrong with the Poole model in Figure 1, as a tool for understanding how the Fed implements policy:

Reserve balances have a special purpose, in that they’re used, intraday, as settlement balances by financial institutions with reserve accounts. But, though the volume of transactions that occurs over Fedwire in a day is enormous, those transactions can be carried out with a very small quantity of total reserve balances, that is the velocity of intraday reserves was humongous when the corridor system was in place. But overnight excess reserves were essentially zero and, since the Fed has now removed reserve requirements (they did it on March 26, 2020) if we had a corridor system today, it would run with essentially zero overnight reserve balances. In Canada, for example, the pre-March 2020 floor system typically always had overnight reserve balances of essentially zero, in a system with no reserve requirements. So, it doesn’t make much sense to be modeling a demand for overnight reserves when overnight reserves are zero. That is, under a corridor system, IOER is set below the target overnight rate so that banks don’t want to hold the reserves overnight. Basically, it makes more sense to think about Fed intervention in a corridor system in terms of the overnight credit market.

It’s actually not easy for the Fed to run a floor system. In fact, as I intend to show you, the Fed’s floor system actually requires active intervention on most days, and in some cases much more intervention than was the case pre-financial crisis.

Part of what is weird about the Figure 1 model is that it does not capture what the Fed actually does in a corridor system to peg the fed funds rate. The Fed did not intervene directly in the fed funds market pre-2008, it intervened by way of the repo market, varying secured lending in the repo market day-to-day. The idea is that for financial institutions with reserve accounts - a reserve account is of course required to participate in the fed funds market - overnight repos and participation in the fed funds market are close substitutes. Though the fed funds market is unsecured, the repo market is secured (the borrower posts collateral), and the repo market has more participants and higher trading volume. But, the idea was that, by intervening in the repo market, the Fed could guide the fed funds rate - albeit without observing the fed funds rate (not actually a rate, but a whole distribution of interest rates on any given day) while the intervention was happening. So, if the repo market was so important for intervention, why aren’t we thinking in terms of an overnight credit market instead of a market for reserves? And note that the repo market also plays an important role in the floor system, which we’ll get to.

An Alternative Approach

I’ll construct a different model. This will be quite crude. It’s going to leave out general equilibrium implications - for example how actions by the Fed matter for macro aggregates such as inflation, employment, and real GDP. But, if we want to think about Fed intervention in the daily overnight market, the approach I’ll take seems OK. Perhaps more important is that we’re going to leave out details of the the structure of overnight markets - over-the-counter and intermediated trades - as well as the market for Treasuries, and I’m not going to be explicit about bank regulation, which is going to be important here. So, some of this is suggestive, and it’s going to be more informative to work this out formally, with the details. That’s for later.

Corridor System

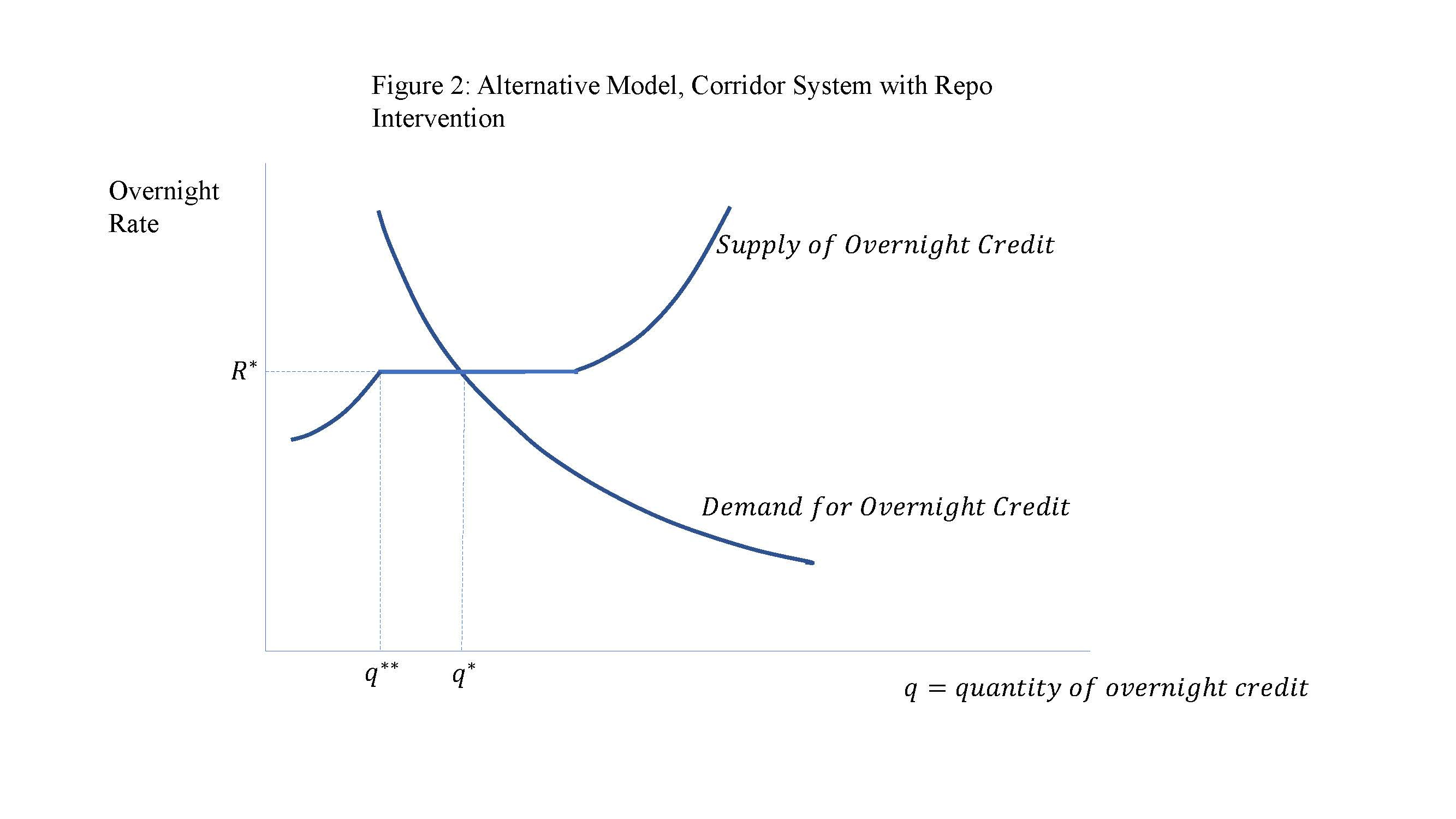

First, I’ll try to capture how the Fed pegged the overnight rate prior to the financial crisis. I’m going to ignore the difference between repos and fed funds lending and borrowing, and just refer generally to the “overnight rate” in an overnight credit market in which all financial institutions can participate. Figure 2 shows a supply curve and demand curve, capturing the behavior of overnight market participants. The trick for the Fed in this corridor regime was to assure that excess reserves were essentially zero overnight, by making sure that the overnight market cleared above the zero nominal interest rate on reserves, and hopefully close to the target overnight rate, given by the FOMC directive. So, the Fed did this by purchasing outright a quantity of (mostly) Treasury securities that would be just short of backing the quantity of currency demand at market rates, and then fine-tuning the supply of overnight credit by essentially supplying a perfectly elastic quantity of repos at the target overnight rate.

In terms of Figure 2, the demand curve (and supply curve too) would be shifting day-to-day, due to shocks to the market, and then repo lending would vary each day to peg the overnight interest rate. For example, in Figure 2, the target overnight rate is R*, and the Fed is supplying q* - q** repos. One important point is that the Fed could have made life easier for itself if it had targeted a repo rate rather than the fed funds rate. This could have been done by auctioning funds at R*, with uptake determined endogenously, much like with the overnight repurchase agreement facility currently in place at the New York Fed.

That is, arguing that a floor system is far easier to run than a corridor system, as for example Bill Dudley did in the passage from his 2018 speech above, is a false comparison. The New York Fed could change its approach by targeting a repo rate - the secured overnight financing rate (SOFR) for example - in a corridor system, and this would be very straightforward.

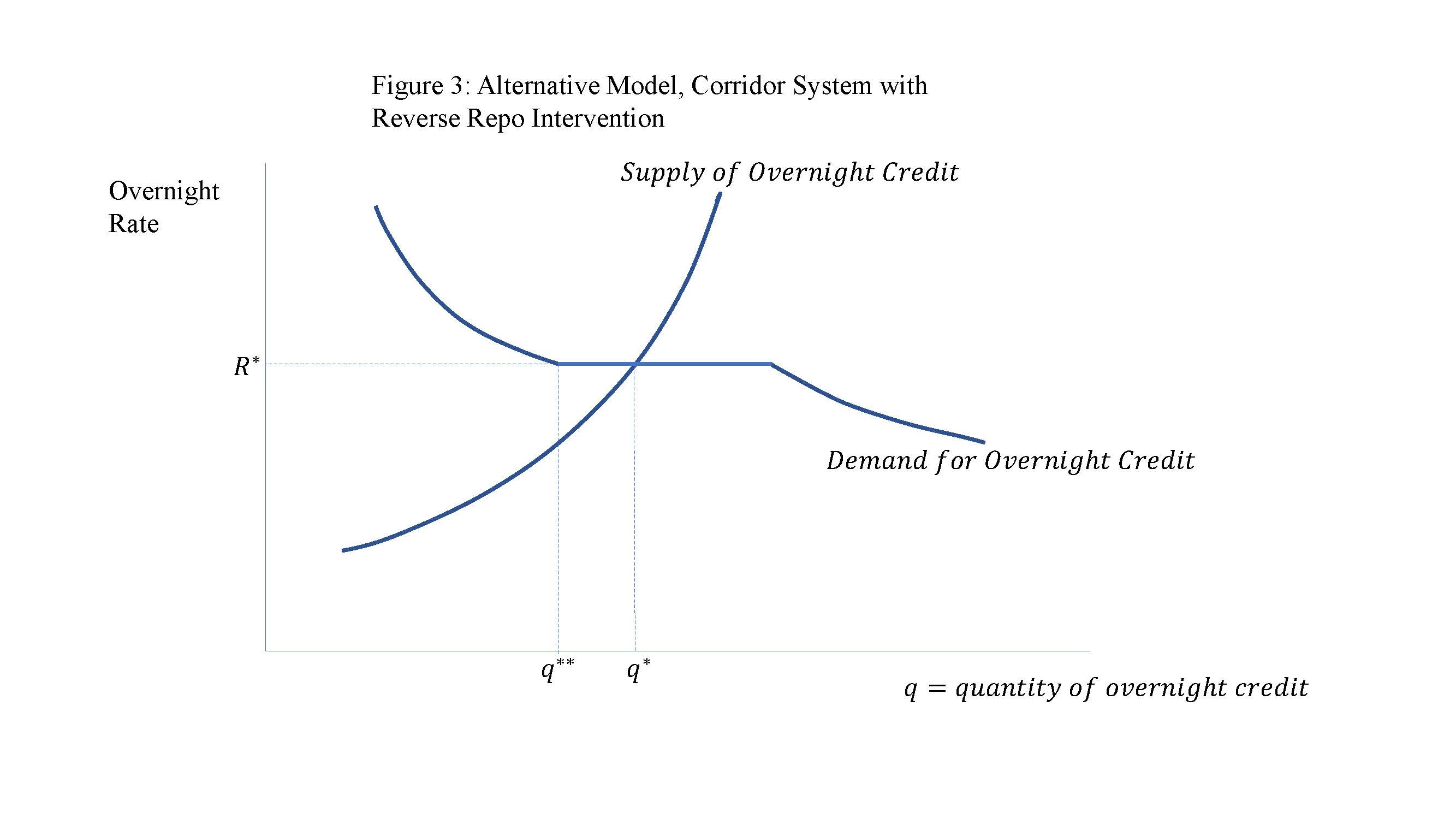

Another approach to pegging the overnight rate in a corridor system is to use reverse repos to fine tune policy each day. In this case, the Fed purchases a quantity of government securities that exceeds currency demand at market interest rates, then makes up the difference with reverse repos, which are then varied day-to-day to accommodate shifts in demand and supply.

In Figure 3, the target overnight rate is R*, and on the day depicted the Fed intervenes by auctioning off q* - q** reverse repos at the New York Fed’s ON-RRP auction. Essentially, there’s not much to choose between repo intervention and reverse repo intervention - the Fed is just on a different side of the market in the two cases. One could even imagine a setup where, on some days, the Fed has repos outstanding, and on other days has reverse repos outstanding. But, in general, reverse repos by the Fed push up the overnight rate and repos push down the overnight rate

Floor System

I’ll start by assuming a frictionless world. Then, we’ll look at features of the data since the Fed’s floor system has been in place, which clearly indicate that this floor system does not work as a frictionless theory tells us it should. Then I’ll discuss what seem to be the key frictions at work, and we’ll sketch out how the alternative theory addresses what is going on in the data.

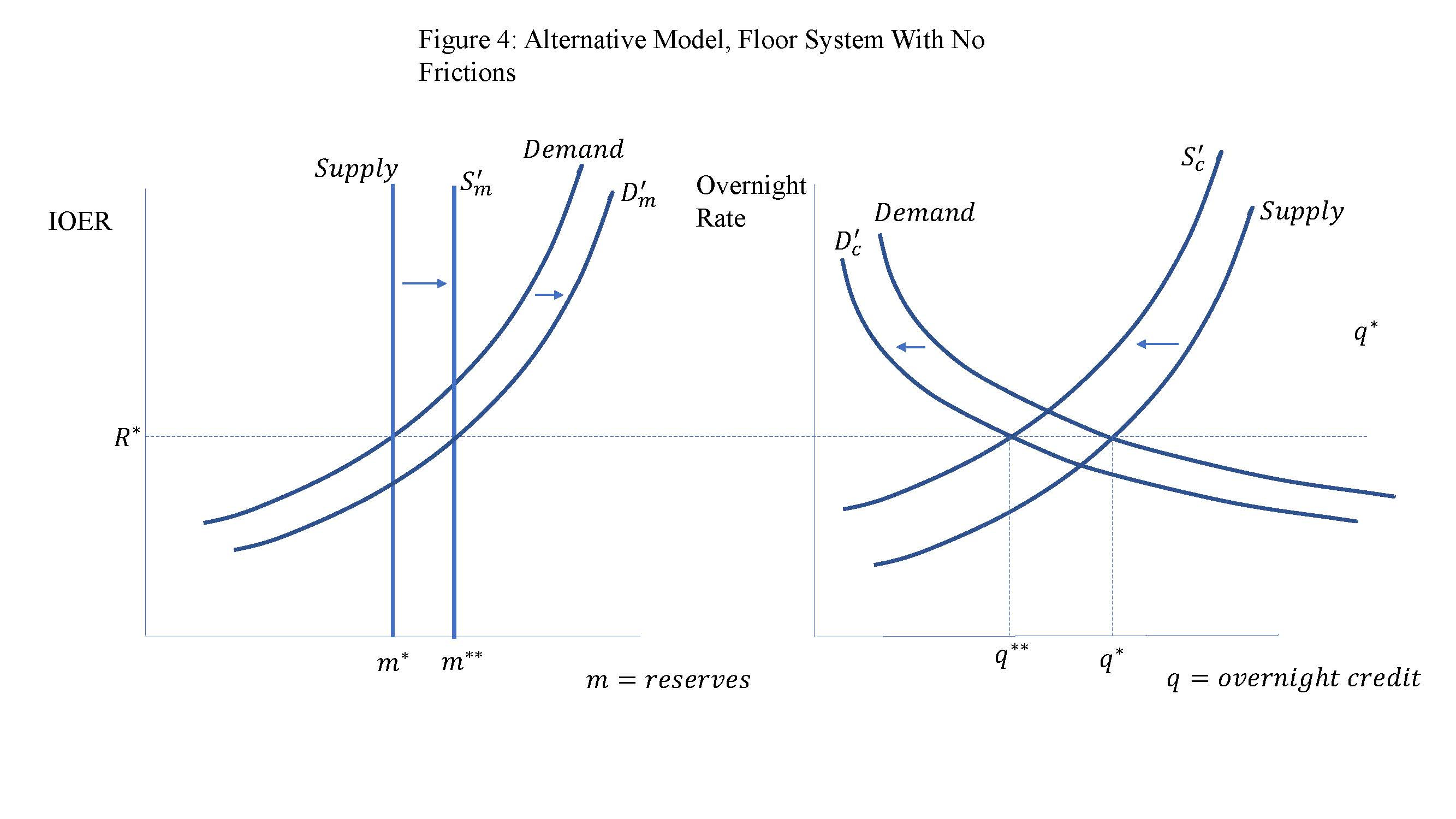

Now we’ll be dealing with two markets. In the left panel of Figure 4 is the market for reserves. That’s an asset market. There’s an inelastic supply of reserves, and banks have an upward sloping demand curve for reserves, given that the variable in the vertical axis in the left panel is IOER. In the right panel of Figure 4 is the overnight credit market, as before. So that’s the flow of overnight credit on a given day - upward sloping supply curve and downward sloping demand curve, with the overnight interest rate on the vertical axis. Again, we’ll ignore the distinction between secured and unsecured lending in the overnight market, but in terms of empirical counterparts, it’s most useful to think of the overnight rate in the model as the repo rate in reality.

First, we have to address what actually pushes the system into floor mode from corridor mode. To see this, go back to Figure 2, and recall that it’s the repo facility at the Fed that pushes the overnight rate down. So, in the figure, suppose that the Fed reduces R* to IOER through repo intervention (so the flat part of the supply curve is at IOER). And suppose that, given R* = IOER, the demand for currency is exactly backed by the assets in the Fed’s portfolio (assuming no Fed capital). That’s the tipping point. Given those settings, if the Fed buys more assets, given R* = IOER, then that requires an increase in reserves.

Next, we want to understand what’s going on in Figure 4. At this stage we’re assuming that there are no frictions that inhibit arbitrage in the overnight market, so in equilibrium the overnight rate is R*, which is equal to IOER. And, given that interest rate configuration, the markets for reserves and overnight credit clear. The quantity of reserves is m*, and the volume of overnight credit is q*.

So, suppose in Figure 4 that the Fed proceeds to buy more assets (this is QE of course), and the supply of reserves increases to m**. This puts upward pressure on the interest rate on reserves, as banks want to receive higher remuneration to hold the extra reserves. But of course the Fed has set IOER at R*. So something else has to adjust. Here I’ll take some liberties. It’s a bit hard to do this with supply and demand curves, without having worked out a more serious model, but here goes. Since banks will be holding more reserves in equilibrium, which are overnight assets, this should diminish the demand for overnight credit. As well, if the Fed purchased Treasuries to increase reserves, that could reduce the demand for overnight credit as there is less safe collateral available. The supply of credit also falls, as banks are now lending to the Fed by way of reserves rather than lending overnight to other financial institutions. Further, the demand for reserves rises, as arbitrage in part works through non-banks that can’t hold reserves lending to banks which hold reserves. The market equilibrates when both markets clear. Reserves rise to m**, and the volume of overnight credit falls to q**.

How’s the Floor Been Working?

The problem, either with the Poole model in Figure 1, or my alternative frictionless model in Figure 2, is that neither is consistent with what we’ve been observing since the financial crisis, with the floor in operation in the U.S.

I’ll start with observed quantities:

Figure 5:

Figure 5 shows repo activity on the Fed’s balance sheet, reverse repo activity, and the quantity of reserve balances. The latter is on a different scale (right hand) so you can see what’s going on. In the reserves time series, there are several important events:

Successive rounds of QE that increase reserve balances after the financial crisis, with QE phased out by late 2014.

Reinvestment continued after late 2014, whereby maturing assets were replaced in the Fed’s portfolio continued. Reinvestment was phased out by October 2017.

After reinvestment stopped, reserves declined until fall 2019, when asset purchases recommenced.

Then the pandemic happened, QE started again, and reserves are now close to $4 trillion, about double the previous peak in 2015.

A key takeaway from Figure 5 is the active intervention that occurred both before and after liftoff (the beginning of conventional policy rate tightening) in December 2015. You can see that ON-RRP intervention (red in Figure 5) began before liftoff. It’s clear the Fed people understood that the floor system wouldn’t quite work, and that ON-RRP intervention would be required for confident targeting of overnight interest rates. But ON-RRP volume declines significantly beginning in late 2017, and then sits at a relatively low level from early 2018 until the pandemic hits in Spring 2020. During that period, another thing happens, which is that Fed intervention begins in a major way on the other side of the repo market. In fall 2019, the Fed began intervening in a big way by lending in the repo market (blue in Figure 5). That continued into the pandemic, and then Fed repos went to zero in mid-2020, and stayed there. Then, the Fed began intervening on the borrowing side of the repo market in early 2021. Since then, ON-RRP volume has steadily increased, and has exceeded $800 billion - a massive amount for Fed repo market intervention historically - in late June 2021.

So, in either the Poole model in Figure 1, or my alternative model, with no frictions, in Figure 4, intervention in the overnight repo market - on either side of the market - should not be necessary. The whole idea behind “easy” floor systems is that, with a large stock of excess reserves outstanding, all the Fed should have to do is set IOER, and that should peg overnight interest rates.

So, what’s going on? As a start in figuring that out, note the following regularities in Figure 1. First, the drop in ON-RRP activity in early 2018 is associated with the phasing out of asset purchases by the Fed. That is, the flow of asset purchases by the Fed seems to be important. Maybe the stock of assets held by the Fed is important too, or it matters what quantities of Treasuries by maturity are held by the public. You can see that in what happens in Fall 2019. In September 2019, Fed asset purchases are still zero, but the stock of reserves becomes sufficiently low at that point that the Fed feels a need to start intervening by doing repo lending every day. Then, by mid-2021, Fed asset purchases have continued at such a high volume, and the stock of reserves is so large that the Fed has to intervene massively through its ON-RRP facility to hold up overnight rates.

Another key element in the story is what was happening with the Treasury’s General Account (TGA), which is another Fed liability:

Figure 6:

Every central bank has to worry about where the central government holds its cash. That is, tax revenue does not come to the government as a constant flow, the government does not spend in a constant flow, and government debt is issued in bunches. So, the federal government needs a cash buffer - a deposit balance that is held somewhere. But if that balance is held with the central bank, that’s going to interfere with monetary policy. Why? If the TGA balance goes down by a dollar, that increases reserves held in the private sector by a dollar, so that works just like an open market purchase of government debt. There are different ways for a central bank to deal with this. In the US before the financial crisis, standard practice was to park the Treasury’s cash in private financial intermediaries, with the TGA balance close to zero at all times. In Canada, when the Bank of Canada ran a corridor system, part of daily BoC intervention involved auctioning off government of Canada cash balances in the repo market.

But, if you think that the floor system works like the Poole model in Figure 1, you would think the TGA balance was irrelevant, as long as it didn’t grow to absorb most of the stock of reserve balances. That seems to have been the view at the Fed and the Treasury post-financial crisis, as the TGA balance grew by a large amount post-2008, as you can see in Figure 6. Then, during the pandemic, the TGA cash balance buffer became enormous by historical standards, peaking at about $1.8 trillion in mid-2020, in Figure 6. Why the Treasury felt it needed such a large buffer is not clear. But, note that the decline in the TGA balance beginning in early 2001 seems to have helped trigger the large increase in ON-RRP volume, through the increase in reserve balances that you can see in Figure 6. So, the large TGA balance during the pandemic presumably just postponed the increase in ON-RRP uptake that would have otherwise occurred earlier.

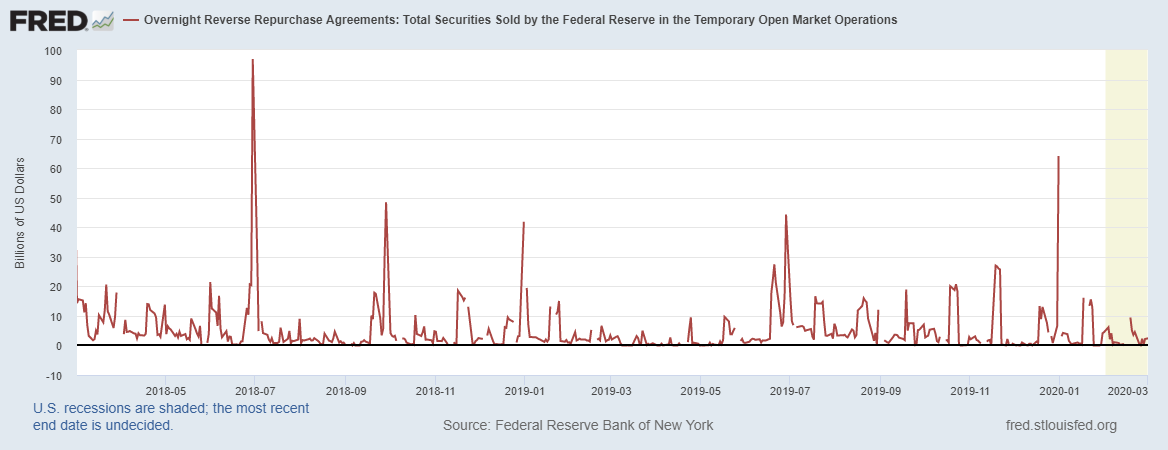

Finally, even in the period from early 2018 to early 2020, there is still significant activity in the ON-RRP facility, if you look at it on a different scale:

Figure 7:

Compare that to the intervention in the repo market that happened before the financial crisis, in 2007:

Figure 8:

The latter is weekly data. Note that Figure 8 shows us the weekly variability needed in the Fed’s corridor system to peg the fed funds rate, and Figure 7 shows us daily intervention that occurred under the floor system, when supposedly such intervention was unnecessary.

To get a clearer picture of what is going on, we need to look at overnight market interest rates as well. Here’s data for the period after liftoff, 2016-2018:

Figure 9:

I’m not showing you a repo rate, as we don’t have easily accessible data that’s equivalent to SOFR (secured overnight financing rate - now a standard repo rate measure) for that period. Instead, Figure 7 shows IOER (green), the fed funds rate (blue), and the 4-week T-bill rate (red). Over a good part of that period, at least until early 2018, the ON-RRP rate, i.e. the rate at which ON-RRP funds are auctioned off, was set at 25 basis points below IOER. A typical pattern, until early 2018 was IOER > fed funds rate > T-bill rate. If we think of the 4-week T-bill rate as a proxy for the overnight repo rate, effectively the ON-RRP rate was pegging the the overnight repo rate, from liftoff until early 2018. That is, it looks as if the Fed were targeting the repo rate, and the public language about fed funds rate targeting within a band was all smoke and mirrors. For example, note the downward spike in the fed funds rate, at the end of each month, until early 2018. Those spikes are due to some financial institutions making end-of-month balance sheet adjustments, which affected the overnight market - a predictable disturbance that would be offset by intervention in a corridor system, and which the floor system is supposed to correct on autopilot.

[Continued in Part II]